By: Thejaswini M A

Translated by: Block Unicorn

Introduction

There exists a category of companies that profit when global conditions deteriorate—defense contractors, oil majors, and gold mining firms. These are obvious examples whose business models are built on instability—and price that instability into their valuations.

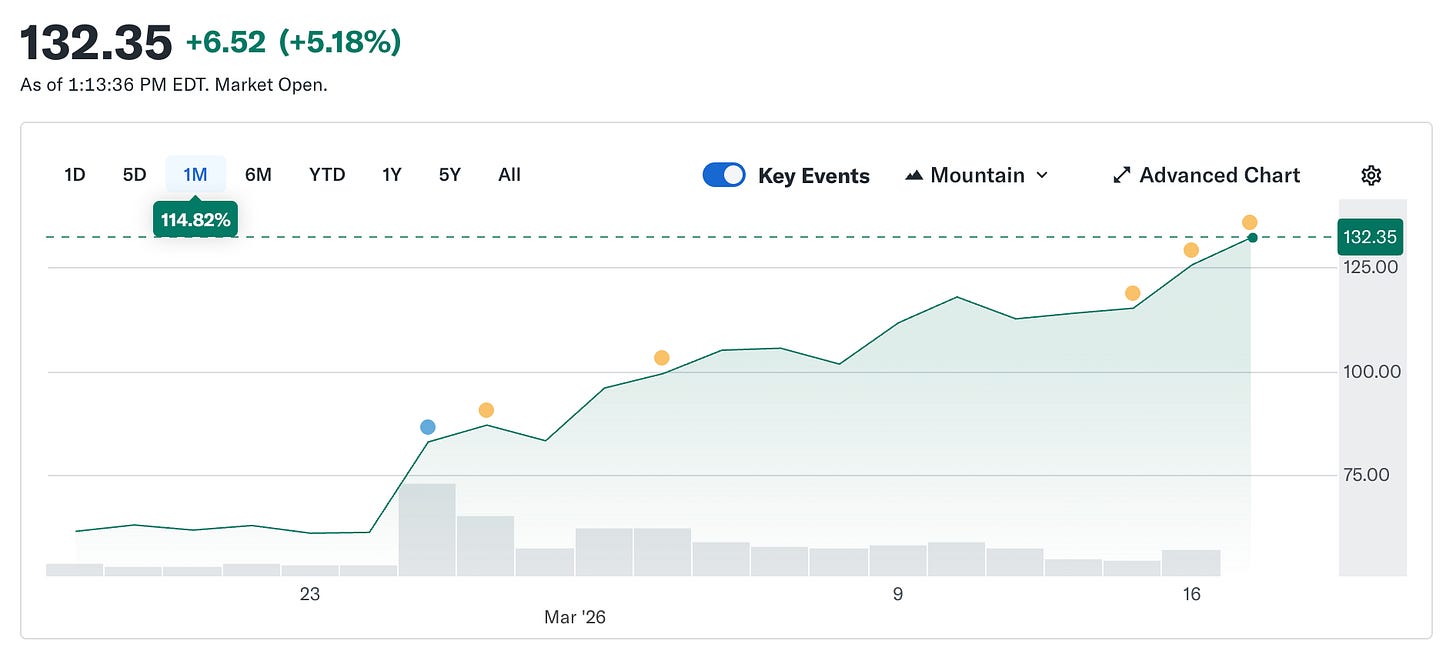

Circle was never supposed to belong in this group. Its token is designed to maintain a fixed value of $1—by design. Stability is the core of its product. Yet Circle’s stock price has surged from $49.90 on February 5 to roughly $123 today—a more-than-doubling in just five weeks—while the broader cryptocurrency market remains 44% below its October peak.

Amid escalating global turmoil, a company whose product is engineered for price stability has become the hottest trade in the market.

I want to explain how it works, why it’s more interesting than it appears, and what it reveals about the distinction between Circle’s fundamental nature and what the market is currently paying for.

What Is Circle? (Yes, we’ll return to this.)

Strip away the branding, the payments narrative, and the infrastructure talk, and you’ll find Circle’s essence: it holds U.S. Treasury securities. Every dollar of USDC in circulation is backed by one dollar of short-term U.S. government bonds. The interest generated by those bonds accrues to Circle—accounting for approximately 90% of the company’s quarterly revenue. Its business model is, in fact, quite simple: Circle is a stablecoin-issuing money market fund.

That means Circle’s revenue depends on a single critical variable: the federal funds rate. When rates are high, Treasury yields rise, and Circle earns more per USDC issued. When rates fall, revenue declines. Everything else is secondary.

Here’s the sequence of events that drove Circle’s stock up 150% from its February low:

Since February 28, the Iran conflict has pushed oil prices up ~35%. Oil above $100 triggers inflation concerns—and inflation concerns mean that any Federal Reserve rate cut would be viewed as reckless. The March 18 decision to hold rates steady was never in doubt. Even before the war erupted, CME’s FedWatch showed over a 90% probability of no change. What the war truly altered was the full-year market outlook. Pre-conflict, markets priced in two 25-basis-point cuts in 2026. Post-conflict, that expectation dropped to just one cut—not before September at the earliest—and the probability of zero cuts in 2026 nearly doubled. With rates expected to stay elevated longer, Circle’s Treasury portfolio yields continue rising—higher yields mean higher revenue; higher revenue means higher stock price. War breaks out—and a stablecoin issuer profits. It caught everyone off guard.

For context, Circle’s February low of $49 reflected pessimistic expectations around rate cuts. Markets anticipated multiple Fed cuts in 2026, which would directly compress Circle’s reserve income. A rough estimate: with current USDC supply at $79 billion, each 25-basis-point cut would reduce Circle’s annualized revenue by $40–60 million. Two cuts would slash revenue by nearly $100 million by year-end. But the war flipped that script overnight—not because Circle changed, but because the macroeconomic backdrop that had supposedly undermined the thesis no longer applied.

How the Squeeze Started

While the rate story kept the stock elevated, the initial explosive move stemmed from positioning.

Ahead of its Q4 earnings release on February 25, ~17.8% of Circle’s float was shorted. Hedge funds had built massive short positions. Their logic: rates would eventually fall, reserve income would shrink, and the company lacked any non-rate-dependent floor of minimum revenue. Fundamentally, that argument seemed sound. Then Circle reported EPS of $0.43—well above the consensus estimate of $0.16—and revenue of $770 million, beating expectations of $749 million. On-chain USDC transaction volume approached $12 trillion this quarter, up 247% year-on-year. Shorts covered en masse. The stock jumped 35% in a single trading day. According to 10x Research, hedge funds lost ~$500 million on short positions in one day. That short squeeze intensified further, extending the post-earnings momentum.

The Coinbase Problem

Here’s the part left out of the bullish narrative.

Circle posted a $70 million net loss in 2025—not a profit. Its Q4 performance was strong, but its full-year results were weak. To understand why, you need to understand the Coinbase agreement—the single most important yet most overlooked element of Circle’s business.

When USDC launched in 2018, Circle and Coinbase formed a joint consortium to govern it. That consortium dissolved in 2023, granting Circle full control over USDC issuance. However, Coinbase retained a revenue share.

Coinbase takes 100% of the yield generated from USDC reserves held on its platform—and splits everything else 50/50 with Circle. In 2024, this arrangement sent $908 million of Circle’s total distribution costs ($1.01 billion) straight to Coinbase. Roughly 54 cents of every dollar Circle earns flows to a company that issues no tokens and holds no reserves. By early 2025, Coinbase-held USDC represented 22% of total supply—up from 5% in 2022. The more USDC grows on Coinbase’s platform, the more Circle earns.

The agreement auto-renews every three years, and Circle cannot unilaterally exit it. The outcome of the next renegotiation will directly impact Circle’s margins. In Q4 2025 alone, distribution costs hit $461 million—a 52% year-on-year increase. The $70 million net loss for the full year was partly driven by a one-time $424 million IPO-related equity compensation expense, making the GAAP loss worse than underlying business performance. Yet Circle’s core business still faces structural cost pressures—problems no interest-rate environment can fully resolve.

The market is pricing Circle as infrastructure. Meanwhile, its P&L shows it’s a rate-trade company burdened by high distribution costs. Both views can coexist—just with different valuation frameworks. Right now, the market is paying for the best version of both.

What makes this more than just a macro trade?

USDC supply recently hit an all-time high of $79 billion—even as the broader crypto market remains 44% below its October peak. This divergence warrants attention. Speculative assets typically decline during market downturns. USDC’s continued growth reflects its use as a vehicle for moving funds—not as a speculative holding. During the Iran conflict, demand for USDC spiked across the Middle East precisely because traditional banking channels became unreliable. When normal payment rails break down, people turn to USDC for remittances and cross-border transfers. That’s infrastructure under stress: usage increases—not decreases.

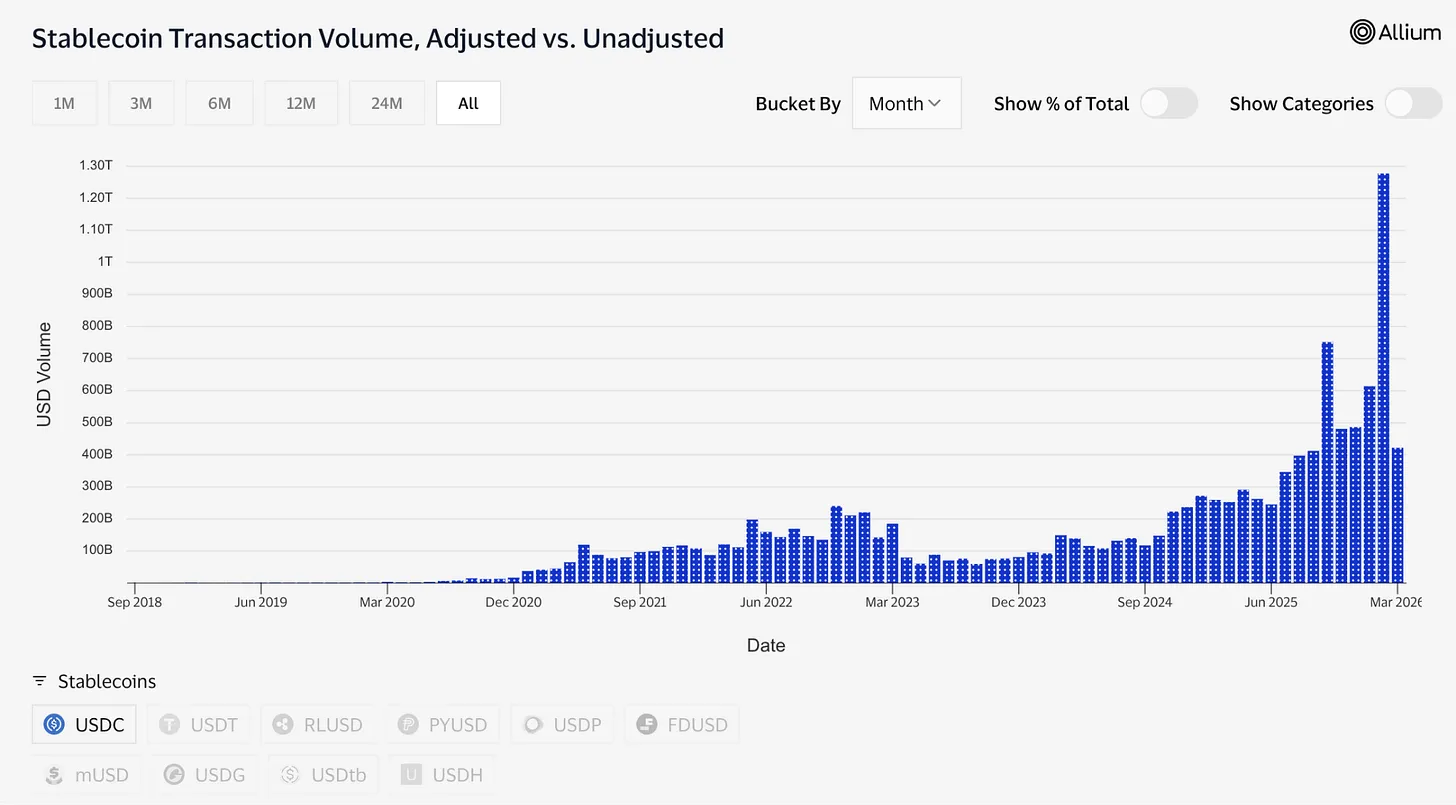

Transaction data confirms this. In February alone, USDC’s adjusted transaction volume reached ~$1.26 trillion, compared to $51.4 billion for USDT. Tether’s market cap remains $18.4 billion—more than double USDC’s $7.9 billion. In terms of total supply, the gap is wide. Yet USDC’s transaction volume has already surpassed USDT’s.

“Dormant supply” and “active settlement” are two distinct concepts. The former refers to where people store capital; the latter refers to the funds people use when they need to move value.

Stanley Druckenmiller offered an insightful take this week. In a Morgan Stanley interview recorded on January 30 and released earlier, he predicted that the global payments system will run on stablecoins within the next 10–15 years—and called crypto “a solution looking for a problem.” The world’s most authoritative macro investor cleanly bifurcated crypto: stablecoins are inevitable infrastructure; everything else is still searching for justification. That framing is the intellectual bedrock of the bull case for crypto.

The Infrastructure Bet

Tokenized assets have grown from ~$1.5 billion at the start of 2023 to ~$26.5 billion today. Many of these products—including BlackRock’s tokenized Treasury fund BUIDL (currently holding >$2 billion in assets)—rely on USDC for subscriptions, redemptions, and settlements. Prediction markets alone are projected to process over $2.2 billion in 2025—mostly settled in USDC. Just Polymarket. Visa now supports over 130 stablecoin-linked cards across 50 countries, with an annualized settlement volume of ~$4.6 billion.

Tokenized assets have grown from ~$1.5 billion at the start of 2023 to ~$26.5 billion today. Many such products—including BlackRock’s tokenized Treasury fund BUIDL (currently managing >$2 billion in assets)—depend on USDC for subscriptions, redemptions, and settlements. Prediction markets are projected to process over $2.2 billion in 2025—largely settled in USDC. Just Polymarket achieves this alone. Visa now supports over 130 stablecoin-linked cards across 50 countries, with an annualized settlement volume of ~$4.6 billion.

Circle is also building the infrastructure beneath all of this. The Circle Payments Network connects 55 financial institutions, processing $5.7 billion annually—enabling banks and payment providers to move USDC cross-border and convert directly into local currencies. Circle’s own Layer-1 blockchain, Arc, is purpose-built for institutional use. Its settlement infrastructure does not rely on Ethereum or Solana. While Ethereum and Solana remain too small to materially affect revenue today, they represent strategic future investments—hedges against potential rate declines.

The AI layer, though small in dollar terms, is structurally significant. Circle’s Global Head of Marketing revealed in March that AI agents completed 140 million payments over the past nine months—totaling $43 million. 98.6% of those transactions settled in USDC, averaging $0.31 per payment. Over 400,000 AI agents now possess purchasing power. The dollar amounts remain tiny—but the direction is unmistakable. If AI agents must pay each other micro-fees—below $0.25—for compute, data access, and API calls—at extremely high frequency, they require a payment method that settles instantly and costs nothing. Circle built Nanopayments for exactly this purpose. Nanopayments enables USDC transfers as low as $0.000001 with zero gas fees—transactions are batched off-chain and settled in batches. The testnet currently supports 12 blockchains, including Arbitrum, Base, and Ethereum.

This is what the market is currently paying $123 per share for: a company at the center of tokenized finance, AI agent commerce, cross-border payments, and prediction markets—and benefiting from regulatory tailwinds like the GENIUS Act and the CLARITY Act, potentially passing before summer. Bernstein’s price target is $190; Clear Street’s is $136; and Seaport Global—the Wall Street firm most bullish on Circle—has set a $280 target.

The Lingering Tension

Here, I want to candidly address something bullish narratives often overlook.

Circle’s profitability depends on a high-rate environment. But that isn’t sustainable forever. The Fed will eventually cut rates. When it does, the Treasury yields backing USDC will fall—and Circle’s interest income will shrink accordingly.

Circle knows this well. It’s actively expanding into transaction fees, enterprise services, its payments network, and Arc—all businesses that don’t depend on rate conditions. But these revenues remain negligible today. Reserve income remains paramount.

So you have two fundamentally different theses sitting atop the same stock price—but they aren’t the same investment.

The infrastructure thesis holds that USDC is becoming a real payments pipe: regulated, transparent, increasingly integrated into traditional finance—and its influence is insulated from rate volatility. This view is supported by data: transaction volumes, institutional adoption, Druckenmiller’s commentary, and Macquarie’s description of stablecoins as the foundational layer of global financial infrastructure. If correct, Circle’s valuation looks cheap regardless of rate environment—because its addressable market spans the entire global payments system.

The rate-trade thesis treats Circle as a long-duration bet on persistently high rates—its stock price already pricing in the Fed abandoning aggressive easing. If this thesis drives the valuation, then every basis point the Fed eventually cuts becomes headwind—and the current share price already exceeds fundamentals justified by a normalized rate environment.

Both views are priced in. The war makes it difficult for the market to discern which one dominates.

Perhaps the most important thing to understand about CRCL right now isn’t whether it reaches $190—but whether you’re investing in infrastructure, or in a more sophisticated Treasury yield proxy. The former is a long-term hold; the latter becomes obsolete the moment Jerome Powell changes his mind.

For now, the war keeps both alive. Oil played a pivotal role—and the company’s true value resides somewhere in the gray zone between them: it has figured out how to build a dollar-denominated internet currency—but now must confront how to survive when dollar yields no longer hit 5%.